Understanding the difference between savings and investments is one of the most important financial concepts you can learn — yet it’s also one of the most misunderstood.

Many people use the terms interchangeably, assume one is “better” than the other, or jump into investing before building any savings at all. In reality, savings and investments serve very different purposes, solve different financial problems, and work best together, not in competition. Part of what makes this distinction so important is that the entry points for both are more accessible than most people assume — you don't need large sums to open a savings account or begin investing. For Ghanaians who are new to building wealth, the question isn't usually whether to invest, but where to begin without taking on unnecessary risk. A solid beginner's guide to investing in Ghana can clarify which products are available locally, how returns are taxed, and what level of volatility to expect at different entry points.

This article is written for everyday earners: salaried workers, freelancers, side hustlers, and small business owners who want to make smarter decisions with their money in today’s economy. Whether you’re trying to build financial stability, grow wealth over time, or simply stop living paycheck to paycheck, understanding where savings end and investments begin is essential.

The problem most people face isn’t a lack of income — it’s misallocation. Money meant for emergencies gets locked into long-term investments. Funds needed for short-term goals are exposed to market risk. And as a result, people are forced to borrow, sell assets at the wrong time, or abandon their financial plans entirely.

In this guide, you’ll learn what savings really are, what investments are designed to do, how they differ across risk, access, returns, and time horizon, and — most importantly — how to use both correctly in 2026 and beyond. By the end, you’ll have a clear framework for deciding where your money should go at every stage of your financial journey.

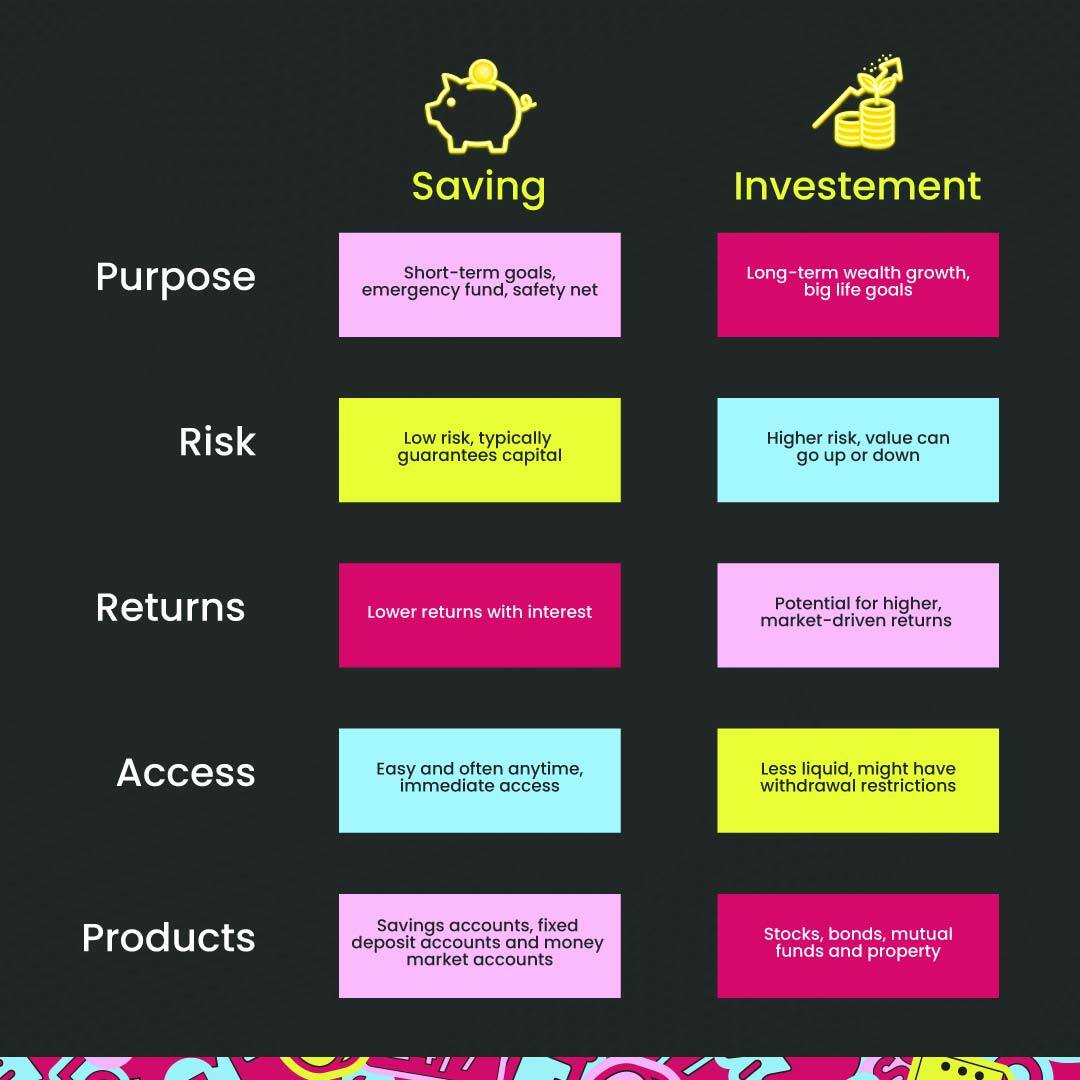

Savings are money you set aside to protect yourself from uncertainty and meet short-term or near-term needs. The primary goal of saving is not to grow rich — it is to stay financially stable.

When you save money, you are prioritizing safety, liquidity, and predictability. Savings are meant to be accessible when life happens: medical bills, school fees, rent gaps, business cash flow shortages, or unexpected expenses that can’t wait.

Savings typically live in low-risk places such as digital savings accounts, traditional bank savings accounts, or mobile-based savings platforms. These options may earn interest, but that interest is secondary to the main function — keeping your money safe and available.

A well-structured savings habit helps you:

If you want a deeper breakdown of savings, this guide on savings accounts and how they work explains it in detail.

Investments are designed for long-term wealth growth, not short-term stability. When you invest, you are intentionally putting your money into assets that can increase in value over time — but may also fluctuate, decline, or take time to recover.

Unlike savings, investments involve risk. That risk is what creates the potential for higher returns. Examples of investments include stocks, bonds, mutual funds, real estate, treasury bills, and managed investment accounts.

The key idea behind investing is this: you are trading immediate access and certainty for future growth.

Investments are best used for goals that are:

If you’re new to this concept, you may find it helpful to read what an investment account is, how investment platforms are structured and why returns vary.

The difference between savings and investments comes down to purpose, not preference. One is not better than the other — they simply do different jobs.

Savings are low-risk by design. Your capital is protected, and the chance of losing your money is minimal. This makes savings suitable for anyone, regardless of income level or financial experience.

Investments, on the other hand, carry varying levels of risk. Market movements, economic conditions, and time all influence returns. While long-term investing tends to grow wealth, short-term losses are possible and normal.

This is why money you cannot afford to lose should never be invested.

Savings are liquid. You can withdraw them quickly and use them immediately. This makes savings ideal for emergencies and daily financial needs.

Investments are less liquid. Some require notice periods, lock-in durations, or selling assets before accessing funds. Even when access is possible, market timing can affect how much you get.

If access speed matters, savings win.

Savings are short-term by nature. They support needs ranging from today to a few years.

Investments are long-term tools. They work best when given time to grow and recover from market fluctuations. Trying to use investments for short-term needs often leads to poor outcomes.

Savings offer modest, predictable returns. The goal is consistency, not maximization.

Investments offer higher potential returns over time, but those returns are not guaranteed. Growth happens unevenly and requires patience.

Understanding this difference helps prevent disappointment and poor financial decisions.

One of the biggest financial mistakes people make is skipping savings and jumping straight into investing. On paper, investing looks more attractive because of higher returns. In reality, this often leads to instability.

When people invest money they should have saved, they end up:

Savings create the foundation that allows investing to work properly. Without that foundation, investments become a source of stress instead of growth.

This is why most financial experts recommend building an emergency fund before committing heavily to investments. If you want to understand this balance better, the article on emergency funds vs savings accounts explains how to structure short-term protection effectively. Once that foundation is in place, the relationship between savings and investment shifts — your savings become the seed capital for longer-term wealth creation rather than just a buffer against emergencies. This is the stage where the type of account you use starts to matter, since different investment vehicles offer different structures for compounding returns over time. Understanding how investment accounts support wealth building helps you move beyond simply accumulating savings and into actively growing them.

The smartest financial approach is explaining how savings and investments complement each other, not compete.

Think of savings as your financial seatbelt and investments as your engine. You need both to move forward safely.

A simple rule many people follow is:

Modern digital savings platforms like Fido’s Easy Save have changed how people save money. Unlike traditional savings accounts that often come with fees or low flexibility, digital savings tools allow users to save small amounts frequently, earn interest, and withdraw when needed.

For example, a digital savings product like EasySave allows users to build a savings habit while keeping their money accessible. This is particularly useful for people with irregular income or those building their first financial safety net.

If you’re exploring savings options, you can learn more about how digital savings accounts work by visiting the Fido Savings page, which explains how modern savings tools are designed for everyday users rather than high-net-worth investors.

Investing makes sense when:

Investing does not make sense when:

Understanding this timing prevents frustration and financial setbacks.

Many financial misconceptions come from oversimplification. One common myth is that savings are “wasted money.” In reality, savings buy you peace of mind and flexibility, which are valuable financial assets.

Another myth is that investing is only for wealthy people. In truth, investing is accessible — but only effective when done at the right time and with the right expectations.

There is also a misconception that you must choose between saving and investing. In practice, successful financial planning requires both.

Your age, income stability, responsibilities, and goals all influence how you should balance savings and investments.

If you are just starting out, prioritizing savings builds discipline and protection. As income grows and stability improves, look toward investing gradually. Over time, your strategy will evolve — but savings should never disappear completely.

For people managing short-term financial gaps, understanding credit options is also important. If emergencies arise before your savings are fully built, learning how personal credit works can help you avoid poor financial decisions while you rebuild stability.

The difference between savings and investments is not about which one is smarter — it’s about using each tool correctly.

Savings protect your present. Investments build your future!!

When you understand their roles and apply them intentionally, you stop reacting to money problems and start planning for financial growth with confidence.

If you approach saving and investing as complementary parts of one financial system, you’ll be far better equipped to handle uncertainty, pursue opportunities, and build long-term financial security.

Savings prioritizes safety and accessibility for short-term needs, typically earning minimal interest in low-risk accounts. Investments aim for long-term wealth growth through assets that can fluctuate in value. Savings protect against emergencies; investments build wealth over time. Both serve different purposes and work best together in a balanced financial plan.

You don't need large sums to begin either. Many savings accounts and investment platforms in Ghana accept small initial deposits, making them accessible to everyday earners. Starting small with consistent contributions is more important than waiting for a large lump sum. Both savings and investments reward discipline over time.

Build savings first. Establish an emergency fund of 3-6 months of expenses in accessible accounts before investing. This protects you from forced early withdrawals or debt when unexpected costs arise. Once your savings foundation is solid, you can begin investing without risking money needed for immediate needs.

Money in savings accounts stays safe and accessible, typically earning small interest rates. Banks hold your funds securely, and you can withdraw anytime without penalties. The focus is protecting your money rather than growing it significantly. Interest earned is predictable and guaranteed, unlike investment returns.

Investments expose your money to market fluctuations because returns depend on asset performance. Stocks, bonds, and other investments can gain or lose value. This variability creates potential for higher returns but also losses. Savings accounts avoid this risk by keeping funds in stable, protected accounts with guaranteed (though lower) returns.

You can, but it's risky. If you withdraw during a market downturn, you lock in losses. Investment funds need time to recover and grow, making them unsuitable for emergency access. This is why separate emergency savings are essential—they provide guilt-free access to money when unexpected expenses arise.

Beginners in Ghana can access mutual funds, treasury bills, stocks, fixed-income bonds, and digital investment platforms. Each carries different risk levels and potential returns. A solid beginner's guide clarifies which local products are available, how returns are taxed, and what volatility to expect at different entry points before committing funds.