The Annual Percentage Rate (APR) is the yearly cost of borrowing money or the yearly earnings from an investment. It is shown as a percentage and includes any fees or extra costs related to the loan or investment. However, it does not include the effect of interest compounding. APR helps you compare the overall cost of loans, credit cards, or investment products from different providers. This single figure is designed to make loan comparison easier — instead of evaluating an interest rate and fees separately, APR combines both into one number that reflects the true annual cost. That's why regulators in most countries require lenders to disclose APR alongside the nominal interest rate; without it, borrowers might underestimate the real cost of a loan with low headline rates but high processing fees. For a deeper breakdown of what APR means and how lenders calculate it, including worked examples, the full explanation walks you through each component.

Interest is the extra amount you pay when you borrow or use something that doesn’t belong to you, like cash, vehicles, or property. In simple terms, an interest rate is the "cost of money"—the higher the rate, the more expensive it is to borrow the same amount.

In Ghana, interest rates apply to most borrowing and lending activities. Individuals borrow money to buy homes, pay school fees, start or grow businesses, or fund other personal projects. Businesses also take loans to expand their operations, such as purchasing land, buildings, or machinery for long-term growth.

The interest rate is applied to the loan amount (called the principal). This interest is the cost of borrowing for the person taking the loan and the income earned by the lender. The total amount to be paid back is usually more than what was borrowed, as the lender needs to be compensated for letting someone else use their money during the loan period. For example, the lender could have used that money for investments instead of giving a loan to earn returns.

When a borrower is considered low risk, such as someone with a stable income or good repayment history, they are usually offered a lower interest rate. On the other hand, borrowers seen as high risk—like those without stable jobs or with poor credit history—are charged higher interest rates.

This makes their loans more expensive since lenders are taking on a greater risk of not being paid back.

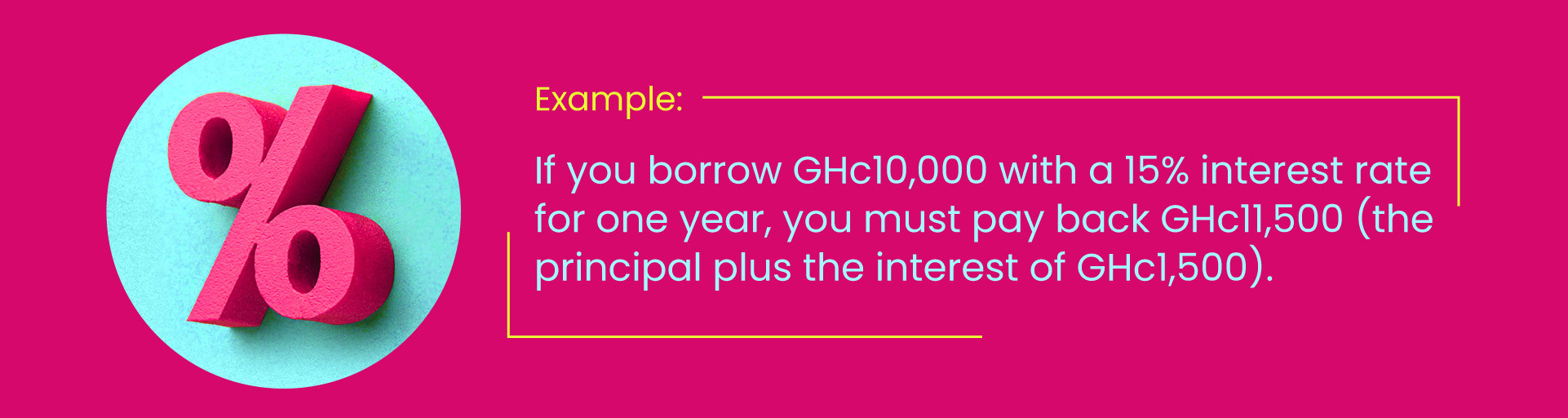

If you take out a loan of GH₵300,000 from a bank, and the loan agreement states that the interest rate is 4% simple interest, you will pay the bank the original loan amount plus the interest. This is calculated as:

Loan amount + (4% × GH₵300,000) = GH₵300,000 + GH₵12,000 = GH₵312,000

The calculation is based on the formula for simple interest:

Simple interest = principal x interest rate x time

The individual who took out the loan will have to pay ₵12,000 in interest at the end of the year, assuming it was only a one-year lending agreement. If the loan was a 30-year mortgage, the interest payment will be:

Simple interest = ₵300,000 x 4% x 30 = ₵360,000

A simple interest rate of 4% annually translates into an annual interest payment of ₵12,000. After 30 years, the borrower would have made ₵12,000 x 30 years = ₵360,000 in interest payments, which explains how banks make money through loans, mortgages, and other types of lending.

Some lenders in Ghana, such as banks and microfinance institutions, may use compound interest instead of simple interest. Compound interest is calculated not just on the principal but also on any interest already accrued. In other words, the borrower pays "interest on interest," which makes the total amount owed higher over time.

For example, at the end of the first year, the borrower owes the principal plus interest. In the second year, the interest is calculated on the new total (principal + first year’s interest). Over time, this significantly increases the amount owed compared to simple interest.

Using the example above, at the end of 30 years, the total owed in interest is almost ₵673,019 on a ₵300,000 loan with a 4% interest rate.

The following formula can be used to calculate compound interest:

Where:

Before taking a loan, asking your lender whether the interest will be calculated using the simple or compound method is essential. This will help you understand how much you will pay over time. Always compare loan offers from banks, microfinance institutions, or savings and loan companies to choose the most favourable terms.

An interest rate is the cost of debt for the borrower and the rate of return for the lender. When you take out a loan, you are expected to pay the entity lending you money something extra as compensation. Likewise, if you deposit money in a savings account, the financial institution may reward you because it can use part of this money to make more loans to its customers.

These charges or payments are called interest and are applied at a specified rate. Explore how you can find the best loan rate with Fido today.

Interest rate is the percentage charged on borrowed money, while APR (Annual Percentage Rate) includes both the interest rate and additional fees or costs associated with the loan. APR provides a more complete picture of borrowing costs, making it easier to compare loan offers from different lenders. This is why regulators require lenders to disclose APR alongside the nominal rate.

Simple interest is calculated using the formula: Principal × Interest Rate × Time. For example, a GH₵300,000 loan at 4% simple interest for one year costs GH₵12,000 in interest. The borrower repays the original amount plus interest. Simple interest doesn't compound, making it straightforward to calculate total repayment amounts.

Banks assess borrower risk based on factors like income stability and credit history. Low-risk borrowers with stable income and good repayment records receive lower rates. High-risk borrowers without stable employment or poor credit history face higher rates to compensate lenders for increased default risk. Higher rates reflect the greater financial risk lenders assume.

Cost of money refers to the interest rate charged for borrowing funds. It represents the price of using someone else's money. A higher interest rate means borrowing is more expensive, while lower rates are cheaper. This cost compensates lenders for forgoing alternative investments they could have made with that money during the loan period.

Using simple interest, a GH₵300,000 mortgage at 4% annually costs GH₵12,000 per year. Over 30 years, total interest equals GH₵360,000. However, most mortgages use compound interest, resulting in higher total costs. Your actual payment depends on the specific interest type, payment schedule, and loan terms offered by your lender.

Compound interest calculates interest on both the principal and previously accumulated interest, while simple interest only applies to the original principal amount. This means compound interest grows exponentially over time and typically results in higher total costs for borrowers. Most modern loans and mortgages use compound interest rather than simple interest calculations.

APR disclosure protects borrowers by revealing the true annual cost of borrowing. Without it, borrowers might be misled by low headline interest rates that hide high processing fees. By combining both elements into one figure, APR enables fair comparison between different loan products and lenders, helping borrowers make informed financial decisions.

.jpeg)