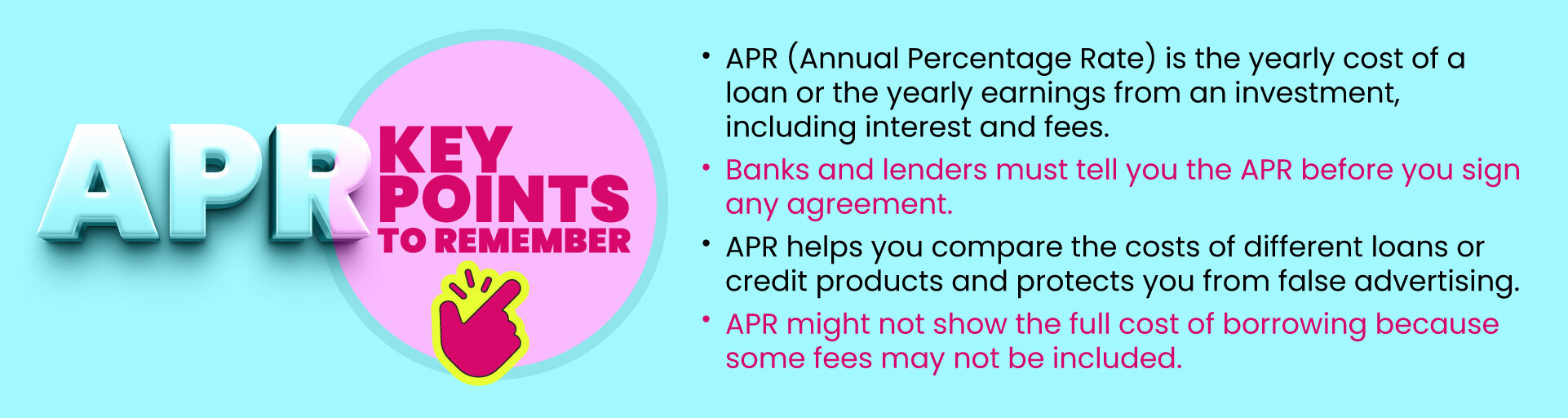

The Annual Percentage Rate (APR) is the yearly cost of borrowing money or the yearly earnings from an investment. It is shown as a percentage and includes any fees or extra costs related to the loan or investment. However, it does not include the effect of interest compounding. APR helps you compare the overall cost of loans, credit cards, or investment products from different providers.

An Annual Percentage Rate (APR) is a way to show how much it costs to borrow money or how much you can earn from an investment in one year. It’s shown as a percentage, so it’s easy to compare.

The APR tells you what percentage of the total loan amount (called the principal) you’ll pay in a year. This includes the interest and fees the lender charges, like processing or service fees. For example, if you take a loan with an APR of 10%, you’ll pay 10% of the loan amount as cost in one year.

For investments, the APR shows the yearly interest you earn on your money. However, it doesn’t include how interest might grow over time when it’s added to your balance (compounding). So, the APR gives a simple idea of what you’ll earn or pay in a year without extra calculations.

In Ghana, regulations ensure that lenders provide clear information to borrowers before entering into a credit agreement. The Borrowers and Lenders Act 2020 (Act 1052) requires financial institutions to disclose key loan terms, such as the interest rate (calculated annually), the total cost of the loan, repayment schedules, and any associated fees.

According to the Bank of Ghana's Disclosure and Transparency Directives for Digital Financial Services, lenders must present all loan-related information in a clear and understandable format. This includes specifying the Annual Percentage Rate (APR) to help consumers compare different loan offers effectively. These directives aim to protect borrowers from hidden costs and promote transparency in the lending process. You can access the detailed guidelines here.

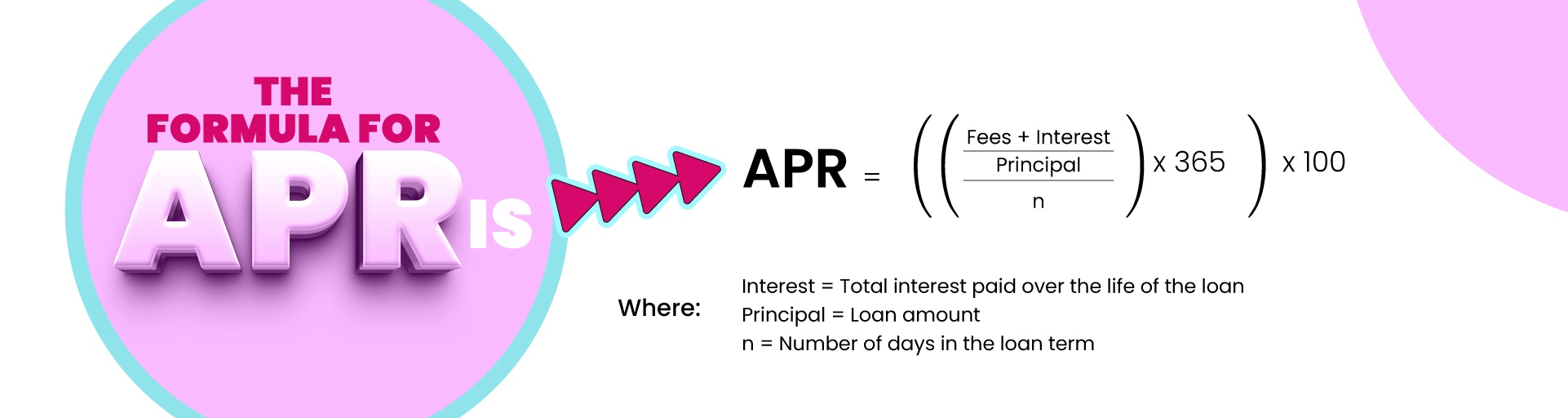

APR is calculated by multiplying the periodic interest rate by the number of periods in a year it applies. It shows the yearly cost of borrowing but doesn’t account for how often the interest is charged to the balance.

Understanding the different Annual Percentage Rates (APRs) types is crucial for making informed financial decisions in Ghana. Here are the main kinds of APRs in Ghana. APR is just one piece of the broader interest rate picture — and Ghana's financial market includes a range of rate structures that behave differently depending on whether you're borrowing short-term or long-term. Fixed rates keep your repayments predictable, while variable rates can shift with market conditions, sometimes in your favour and sometimes not. To see how APR fits into this wider landscape, it helps to understand the full spectrum of interest rate types in Ghana and how they affect borrowers across different loan products.

A fixed APR remains constant throughout the loan term. This means your interest rate and monthly payments do not change, providing stability and predictability in your budgeting. Many personal loans offered by Ghanaian banks come with fixed APRs..

APR variable can fluctuate over time, often linked to the Ghana Reference Rate (GRR) set by the Bank of Ghana. If the GRR increases, your interest rate and monthly payments may also rise. This type of APR is common in products like certain types of mortgages or business loans.

Some financial institutions offer a lower APR for an initial period to attract customers. After this introductory phase, the APR increases to the standard rate. For example, a bank might offer a reduced APR for the first six months on a new credit card.

This APR applies to credit card purchases. If you do not pay off your credit card balance in full each month, the purchase APR is applied to the remaining balance, resulting in interest charges.

If you miss a payment or violate other terms of your credit agreement, your lender may impose a penalty APR, which is typically higher than the standard APR. This increased rate can significantly raise the cost of your debt.

Knowing the type of APR associated with your financial products helps you anticipate changes in your payment amounts and manage your finances effectively. Always review the terms and conditions your bank or financial institution provides to understand the APR and how it can affect your repayments.

In Ghana, financial institutions are required to disclose APRs on their products to protect consumers and ensure transparency. This prevents lenders from misleading customers by advertising lower monthly rates that could be mistaken for annual rates.

Without APR disclosure, a company might promote a lower monthly interest rate, making it harder for customers to compare it accurately with other annual rates. By mandating APR disclosure, customers can compare loans and credit products equally and make informed financial decisions. For more transparency regulations, refer to the Bank of Ghana's guidelines.

What is considered a "good" APR in Ghana depends on several factors, such as current market rates, the base rate set by the Bank of Ghana, and the borrower’s creditworthiness. When the base rates are low, financial institutions may offer competitive APRs.

For example, you might find loans with low APRs or even 0% introductory rates on specific products like car loans. However, checking whether these rates apply throughout the loan term or are promotional rates that increase after a certain period is essential.

Low APRs are often reserved for borrowers with strong credit histories or stable incomes. Consumers should read the loan agreement carefully and ask questions to understand the terms fully.

Always remember to be responsible when borrowing from any financial institution or bank. You must know your financial capacity before applying for a loan.

Let's watch some fellow Ghanaians explain the reasons why they borrow.

. Explore how you can compare loan rates — try Fido today.

APR includes both the interest rate and additional fees or costs associated with borrowing, while the interest rate alone only represents the cost of the principal. APR provides a more complete picture of the true yearly cost of a loan, making it easier to compare different loan offers from various lenders.

No, APR does not include the effect of compound interest. It shows a simple yearly cost without accounting for how interest compounds over time. If interest compounds monthly or daily, the actual amount you pay may be higher than the APR suggests.

APR is calculated by multiplying the periodic interest rate by the number of periods in a year. For example, if your monthly rate is 0.83%, multiply it by 12 to get the annual percentage rate. This gives you the yearly cost of borrowing without considering compounding effects.

A fixed APR remains the same throughout your loan term, keeping payments predictable and stable. A variable APR fluctuates based on market conditions, often linked to the Ghana Reference Rate. Variable rates can increase or decrease, affecting your monthly payments over time.

APR is important because it shows the total yearly cost of borrowing, including fees and interest. This makes it easier to compare loan offers from different lenders on equal terms. Without APR, comparing loans would be misleading since you'd only see the interest rate.

No, APR and interest rate are not the same. The interest rate is just the cost of borrowing the principal, while APR includes fees, processing charges, and other costs. Under Ghana's Borrowers and Lenders Act 2020, lenders must disclose both to help borrowers understand the true cost.

An APR of 10% means you'll pay 10% of the loan amount as a yearly cost, including interest and fees. For example, on a 1,000 Ghana Cedis loan at 10% APR, you'd pay approximately 100 Ghana Cedis in total costs over one year, though this is spread across monthly payments.